Facebook Deep Dive

Next Stop...$1 Trillion 🚀

In this issue of Moneyball Investing I’ll be covering Facebook (FB). There has been a lot of scrutiny on Facebook as of late. If you are curious about that then you can watch the news 😉 I’ll be sharing why I recently took a position in Facebook, why I am bullish, and how I think the markets are underestimating how big this company can really become.

👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇

Moneyball Investing is a free newsletter breaking down compelling investment opportunities. Subscribe if you are interested in investing in innovative companies and the technologies and products behind them.

👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆

Facebook Intro

Facebook was created in 2004 by Mark Zuckerberg and his college roommates. The company has grown substantially from its roots as a social networking service, and in this newsletter I will be covering Facebook’s entire ecosystem and why I am very bullish about the long term growth prospects of the business.

It is important to note that at the time of this writing I am a Facebook shareholder. We will be covering the company’s business model, family of products, future growth catalysts, and risks (of which, there are many).

Facebook Ecosystem

Facebook has evolved into a multifaceted technology behemoth. Its business can be broken down into the following segments:

Facebook: Enables people to connect, share, discover, and communicate with each other on mobile devices and personal computers. There are a number of different ways to engage with people on Facebook and build community, including Facebook News Feed, Stories, Groups, Shops, Marketplace, News, and Watch.

Instagram: Brings people closer to the people and things they love. It is a place where people can express themselves through photos, videos, and private messaging, and connect with and shop from their favorite businesses and creators. They can do this through Instagram Feed, Stories, Reels, IGTV, Live, Shops, and messaging.

Messenger: A simple yet powerful messaging application for people to connect with friends, family, groups, and businesses across platforms and devices through chat, video, and Rooms.

WhatsApp: A simple, reliable, and secure messaging application that is used by people and businesses around the world to communicate and transact in a private way.

Facebook Reality Labs: Facebook’s augmented and virtual reality product suite. Oculus Quest lets people defy distance with cutting-edge virtual reality (VR) hardware, software, and content, while Portal helps friends and families stay connected and share the moments that matter in meaningful ways.

The magnitude of Facebook’s products and services is illustrated in the table below as the company holds 4 of the top 10 spots for most downloaded apps globally.

Facebook faces fierce competition from other social-based applications such as Snapchat and TikTok. Additionally, monetization efforts in certain geographies such as Asia have proven to be difficult. However, Facebook’s leadership has navigated these challenges and I think the results can be seen in the financials.

Financial Results and Key Performance Indicators 📊

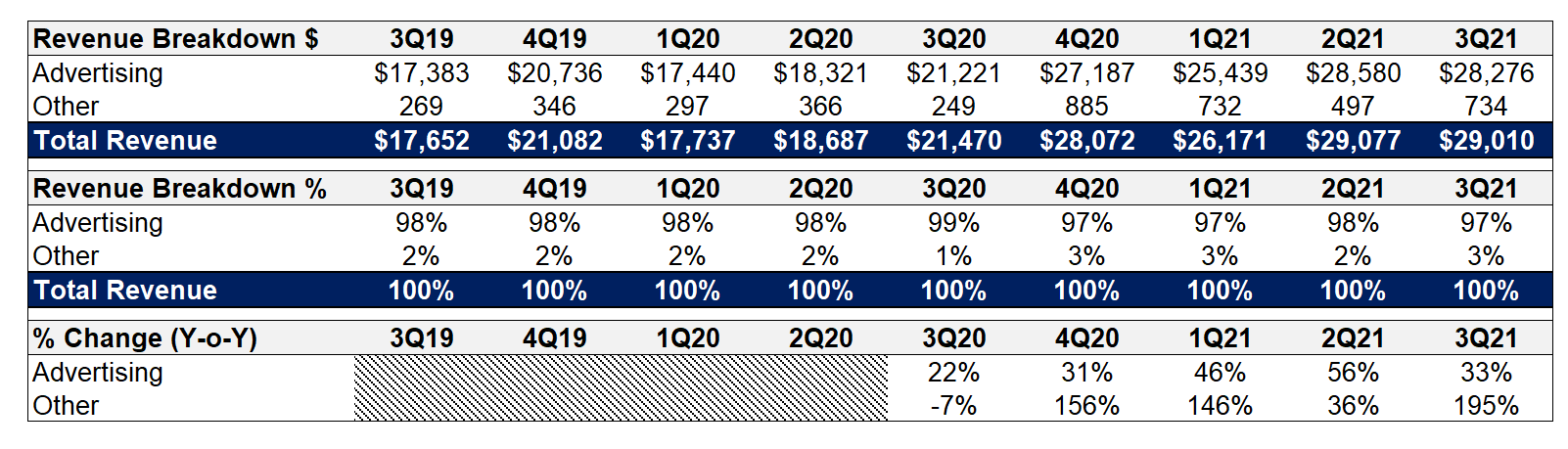

For Q3 2021 Facebook reported $29 billion in revenue, representing a 35% increase year over year. On a YTD basis, Facebook has generated $84.3 billion in revenue, representing 46% year over year growth.

Although the majority of its revenue comes from Advertising, Facebook’s Other Revenue (Oculus, Portal) is growing over 100% year over year and is now a multi-billion revenue stream. Despite the high concentration of its revenue, this growth should not be overlooked. Facebook has been able to generate consistently higher revenue while sustaining expense margins (more on that below). As a result, the company has generated consistent cash flow which it has used to re-invest back into the business in the form of:

New revenue pursuits (e.g. metaverse, e-commerce)

Honing existing product offerings (AR/VR)

Strategic M&A, allowing the company to penetrate underserved markets (FB/Reliance). It’s important to note that two of Facebook’s key growth drivers were acquired (Instagram and WhatsApp). The company has proven that it can identify, integrate, and monetize strategic opportunities into multi-billion dollar businesses.

Share Repurchases

The table above breaks down Facebook’s Revenue by geography and the rate at which these geographies are growing and by which revenue segment. We can see that Facebook is seeing a lot of traction in Europe and Asia-Pacific in both Advertising and Other Revenue. Given the amount of competition the company faces (especially in Asia), I find these trends particularly encouraging. Furthermore, I think this showcases Facebook’s ability to enter and monetize new end markets with multiple products.

Risk Factors 🚨

Regulatory Scrutiny: Facebook CEO Mark Zuckerberg has spent his fair share of time on Capitol Hill answering questions about Facebook, its practices, the role it plays in society, etc.

Mitigant: Although this is a bit of a generalization, the larger something becomes, the more attention it will receive. We have seen leaders from Apple, Google, Amazon, and Twitter all testify before Congress on multiple occasions. Although these testimonies often make for great click-bait for a couple of weeks, very little actually comes from them. From time to time a corporation will be fined, but when it’s all said and done it’s pretty rare that a company is broken up or someone in leadership is effectively forced to resign. When it comes to investing I tend to focus on the metrics, and Facebook is no different. Despite the media coverage, Facebook is growing its core metrics, resulting in higher revenues, higher profits, and greater shareholder returns. As Curtis “50 Cent” Jackson says, “If it makes money, it makes sense.” I plan to continue draining out the short term noise for long term profit taking.

Revenue Concentration: The chart below illustrates that Facebook generates the majority of its Revenue from Advertising. One can see that Advertising comprises about 97% of the Company’s Total Revenue.

Mitigant: Although Advertising comprises the majority of Facebook’s revenue, this revenue stream is consistently growing over 30% year over year. There are very few companies that can generate tens of billions of dollars in quarterly revenue and grow at 30%, especially from a singular product. What may be even more impressive is that Facebook has been able to generate this growth while keeping expenses relative flat as a % of Revenue. The image below highlights that the margin profiles of Facebook’s Research & Development and Sales & Marketing expenses have remained flat, while the company has continued to grow its top-line.

Finally, the company’s Other Revenue segment should not be overlooked. Facebook has made it clear that they will be aggressively pursuing other areas of growth such as Augmented/Virtual Reality software and hardware (Oculus, Portal), as well as e-commerce. Facebook’s Other Revenue segment has been consistently growing in the triple digits year over year. By investing in areas such as the metaverse and e-commerce/payments, which both have large Total Addressable Markets, Facebook will begin diversifying its revenue base. Since Other Revenue accounts for only 3% of Revenue today, there is a lot of opportunity for Facebook’s future growth.

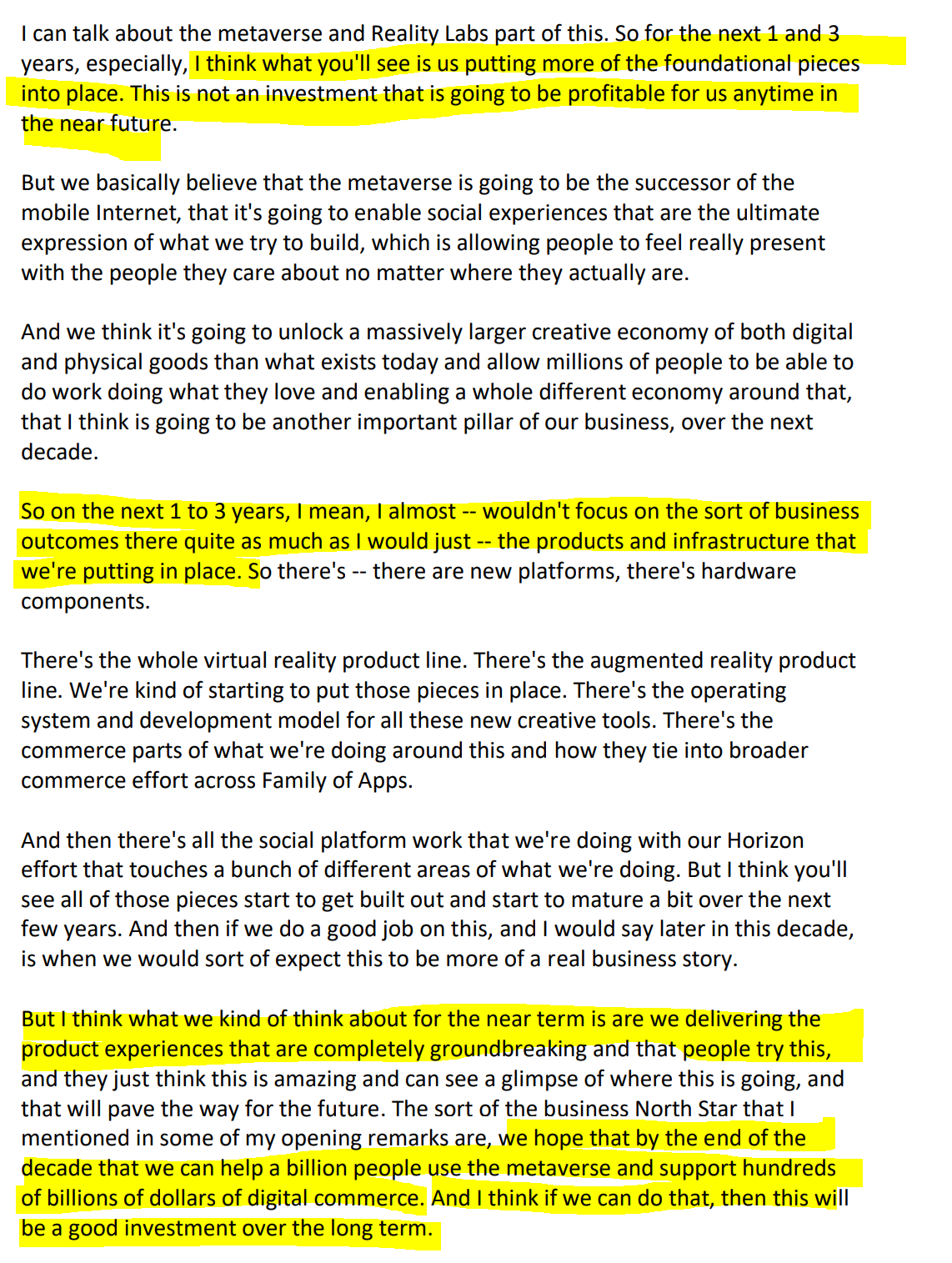

Metaverse Ambitions: Facebook has a keen interest in the metaverse. It is rare that a company that has dominated one particular industry for so long is nimble enough to pivot its focus on something entirely different, and also own that new market. For this reason, some fear that Facebook’s metaverse aspirations may end up as more of a “moonshot” which could potentially fail.

Mitigant: Although we are in the very early innings of these developments there is little doubt that several companies will begin investing heavily and developing products and services for the metaverse. I personally view this as a net positive because competition often breeds the best innovations. Moreover, I think that we need to listen to Zuckerberg and how he views Facebook’s metaverse roadmap. This is not a business that is going to contribute meaningful profits in the short term. It is going to require a lot of expensive engineering, product development, and marketing. For this reason, I think that we need to be thinking about how large the addressable market for the metaverse is, and how well equipped is Facebook to capture a meaningful portion of that market over a long-term horizon. Lastly, although it may be difficult for Facebook to enter and dominate a new market, we have seen other companies successfully pivot before (e.g. Amazon introducing AWS as it looked to diversify from primarily e-commerce). A huge factor in Facebook’s metaverse execution will come down to Management.

The images below are from the Q3 2021 Earnings Call Transcript:

I’ve included a video below of Cramer covering Facebook’s Q3 2021 Earnings and his opinion regarding the company’s ability to enter the metaverse. Take it for what you will with Cramer 🧂🧂🧂

Competition: Facebook faces competition from a number of other companies that provide connection, sharing, discovery, and communication products and services to users online. Moreover, Facebook has faced some existential crises over the course of its history. For example, Snapchat took the world by storm when it was launched in 2011 and there are lots of rumors that Facebook tried to acquire them on more than one occasion. In more recent memory, Facebook has faced a lot of competition from Bytedance owned TikTok, and the Gen Z demographic.

Mitigant: Good artists borrow, great artists steal. As we now, Facebook ultimately never acquired Snapchat. Instead, the company launched its own version of Snap’s image/video disappearing functionality, Instagram Stories. Similarly, Facebook launched “Reels”, which is similar to TikTok. As of Q3 2021, Facebook is sitting on $58 billion of Cash and Cash Equivalents and the company has some of the brightest engineers and product managers on the planet. Facebook is well equipped to take on and ward off competition.

I will admit that the table below is a little misleading. I’ve captured Daily Active Users for Facebook, Snap, and Twitter. Of course, the company faces competition from other companies like Pinterest, Bytedance (TikTok), and Google (YouTube). However, metrics for subsidiaries are tougher to find and sources online can be less reliable. Additionally, the definition of a Daily Active User will differ among companies given the underlying nuances of each business. Lastly, Facebook has been around longer than both of those companies. However, for simplicity and illustrative purposes, we can see that Facebook has 1.9 billion daily actives, significantly above Snap and Twitter.

Leadership 📑

Other Resources 🔍

Q3 2021 10Q Filing: SEC Reporting

Q3 2021 Earnings Presentation: Slides

Q3 2021 Earnings Release: Press Release

Facebook Investor Relations: IR Homepage

My YouTube Channel: Moneyball Investing YouTube

Featured YouTube Video: Couch Investor is someone I’ve been following on YouTube for quite some time. He does a great job synthesizing investment opportunities in the technology space.

Subscribe 👉 Couch Investor

More videos:

🚨 Disclaimer: The stocks mentioned in this newsletter are not intended to be formal recommendations. Rather, this newsletter is for educational and entertainment purposes. I encourage readers to do their own research and conduct their own due diligence before buying any stocks mentioned in my write-ups.

Thank you for reading! 👏Don’t forget to Subscribe and Share! It’s Free! 💸

👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇 👇

Moneyball Investing is a free newsletter breaking down compelling investment opportunities. Subscribe if you are interested in investing in innovative companies and the technologies and products behind them.

👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆 👆