If you have cable television or are too cheap to pay for Hulu without commercials like I am, then chances are you’ve seen commercials for Capital One and their “Banking Reimagined” marketing campaign. Although the intent behind a slogan like “Banking Reimagined” may seem nice on the surface, I think that it can actually do more harm than good. Why? Because it actually causes the audience (potential customers) to ponder “why does banking need to be reimagined?” Because:

Large incumbent banks and financial institutions have been the targets of some of the largest cyber attacks in recent memory

It can take several days for a transaction to post to your online account

The customer service at your bank is (most likely) awful

Banks lack the variety of services or move at the velocity that tech-oriented consumers demand in today’s society

In other words, the legacy banks are standing in their own way by gifting customers a free check book instead of providing them with a suite of products that allow them to do everything they realistically need and want to do, on their time, in an intuitive, mobile-first way. This dynamic has led to fragmentation in the financial services industry, allowing new players to emerge at a frightening pace. One of these newcomers is SoFi.

Product Overview (B2C)

SoFi operates through three segments: Lending, Technology, and Financial Services.

Lending: The company offers multiple loan products, such as student loans, personal loans, and home loans.

Financial Services: SoFi offers a suite of financial services solutions, including cash management and investment services across different products.

SoFi Money: A digitally-native, mobile cash management experience

SoFi Invest: A mobile-first investment platform offering members access to trading and advisory solutions, such as active investing, robo-advisory and cryptocurrency accounts.

SoFi Credit Card: Offers a rewards program that provides double the rewards when the cardholder redeems them into SoFi Money, SoFi Invest, or SoFi personal or student loans.

To complement these products, SoFi offers financial tracking through its Relay product, and partners with other enterprises through loan referrals and its “SoFi At Work” service. They have also developed a financial services marketplace platform branded Lantern Credit to help applicants that do not qualify for SoFi products with alternative products, as well as providing a product comparison experience.

The company’s strategy revolves around a concept that they call “Financial Services Productivity Loop”. The idea is centered around cross-selling its product suite to existing members. For example, a SoFi member may apply for a student loan (product 1). Based on their experience, this member may later consider using a second product (e.g. SoFi invest). As the member uses more SoFi products and becomes more engrained into its ecosystem, SoFi generates more revenue per member without incurring additional member acquisition costs, resulting in higher lifetime value per member.

In addition to realizing the benefits of more members adopting multiple SoFi products, the Company’s strategy delivers operating and technology efficiencies to deliver better unit economics on a per product basis. As a result, SoFi is able to use the increased profits to further improve member benefits and the overall product experience.

As you can in the image above, SoFi has been able to reinvest and launch new products at a staggering rate.

Product (B2B)

In April 2020 SoFi acquired a company called Galileo for $1.2 billion. Galileo operates in the space of Banking-as-a-Service. Its digital payments platform enables checking and savings account-like functionality via its powerful open APIs. This provides companies with an easy way to create sophisticated consumer and B2B financial services.

Galileo’s APIs power functionalities including account set-up, funding, direct deposit, ACH transfer, IVR, early paycheck direct deposit, bill pay, transaction notifications, check balance, and point of sale authorization as well as dozens of other capabilities.

The thesis for this acquisition was to take the SoFi product and wrap Galileo’s enterprise-grade APIs around it, making it available to Galileo’s commercial clients and SoFi’s consumer base. In a way, the SoFi/Galileo combination is analogous to an Amazon/AWS type model. On one side of the equation there is a consumer business, and on the other side there is a technology infrastructure play.

The slide below outlines the strategic rationale for this transaction 👇

Financial Results

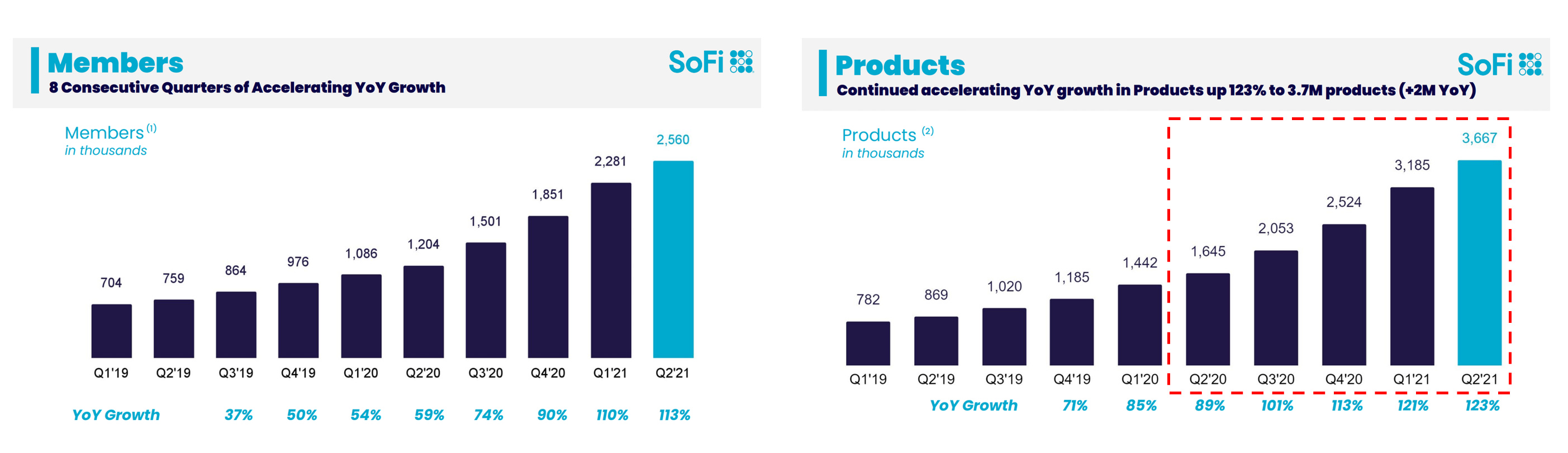

SoFi has delivered 8 consecutive quarters of membership growth. As of Q2 2021, the company reported 2.6 million members, up 113% year over year. Additionally, the Company boasts 3.7 million products, up from 1.7 million just one year prior.

This is an interesting dynamic because we can see in the charts below that SoFi is seeing meaningful growth in both its Lending and Financial Services products. However, what really stands out is the Company’s Financial Services Products has quadrupled from 601k to 2.7mm since the start of the Pandemic.

Growth across the product suite has led to top-line hypergrowth throughout the Company. However, it’s important to note that SoFi is still operating at a loss. As noted above, the Company is using the cash flow from efficient unit economics to invest back into the business. Per the Company’s latest 10-Q, they are investing aggressively in technology and product development as well as sales and marketing (more on that below).

Over the last month, Equity Research analysts from Morgan Stanley, Jefferies, and Mizuho have stamped SoFi with Buy ratings. The analysts note that SoFi’s “Flywheel” business model will continue to drive significant user growth, product adoption, and margin expansion. Unlike traditional banking incumbents, SoFi provides its members with a simple UI/UX with richer APIs (Galileo integration), thereby drawing customers toward ancillary products. These products offer members the speed, selection, content, and convenience that only an integrated digital platform can provide.

In a decade SoFi has evolved from its original loan business to a technology-enabled financial services company and created a ‘Super App’. This is important because as of now the Company’s Loan segment still accounts for an overwhelming portion of its Total Revenue. As members continue to take advantage of of the technology platform and financial services offerings, SoFi’s revenue mix and margin profile will begin to shift. At scale, the unit economics of the member base should improve the profitability prospects of the business as consumers remain sticky.

Bank Charter On The Horizon

SoFi has stated that it hopes to have a bank charter in hand before the end of 2021. This is meaningful because Galileo’s infrastructure can complement obtaining a bank charter, making it easier for SoFi to partner with other companies to offer sweep accounts, FDIC insurance warehouse facilities, among other financial services. Morgan Stanley noted that SoFi's approval of its bank charter could boost total revenues by 10% within its first year solely based on the benefits of gaining access to the same low interest rates as other banks.

Gen Y/Z - Move Your Money Campaign

In late September SoFi announced a new brand campaign, "Move Your Money". The campaign is airing in NFL, College Football, and Broadcast Primetime, and across all major national cable/streaming platforms, with the extension of a digital and influencer campaign.

Although competition is rising among challenger FinTechs for Gen Y & Z, SoFi’s roots stem from the hardest part of consumer finance, lending, along with a robust digital offering. Both of these attributes give them a head start when appealing to Gen Y & Z.

As part of the campaign SoFi is launching a sweepstakes calling on members to share their “money moves” story in a video to Instagram, TikTok or Twitter. Up to ten $1,000 prizes will be awarded per weekly period and one grand prize of $25,000 will be awarded at the end of the contest period. In total, SoFi will pay out up to $75k in prize money. As of the time of this post, the hashtag #SoFiMoneyMoves has been viewed nearly 6 Billion times on TikTok.

Management Team Profiles

Conclusion

As of the time of this post I own roughly 600 shares in SoFi at an average cost of $17/share. I initially purchased shares in IPOE shortly after the IPOE/SoFi SPAC merger was announced. I have averaged down on dips over the last several months. I plan to hold SoFi for the long term as it complements my other positions in the FinTech landscape.